Tokenization <> Alts

For retail, that means breaking through a wall that’s long been built by legacy wealth platforms, outdated rules, and painful onboarding

Been thinking about the real play of tokenization. I see it as giving retail access to alts— and thus a threat to legacy wealth platforms.

In the U.S.:

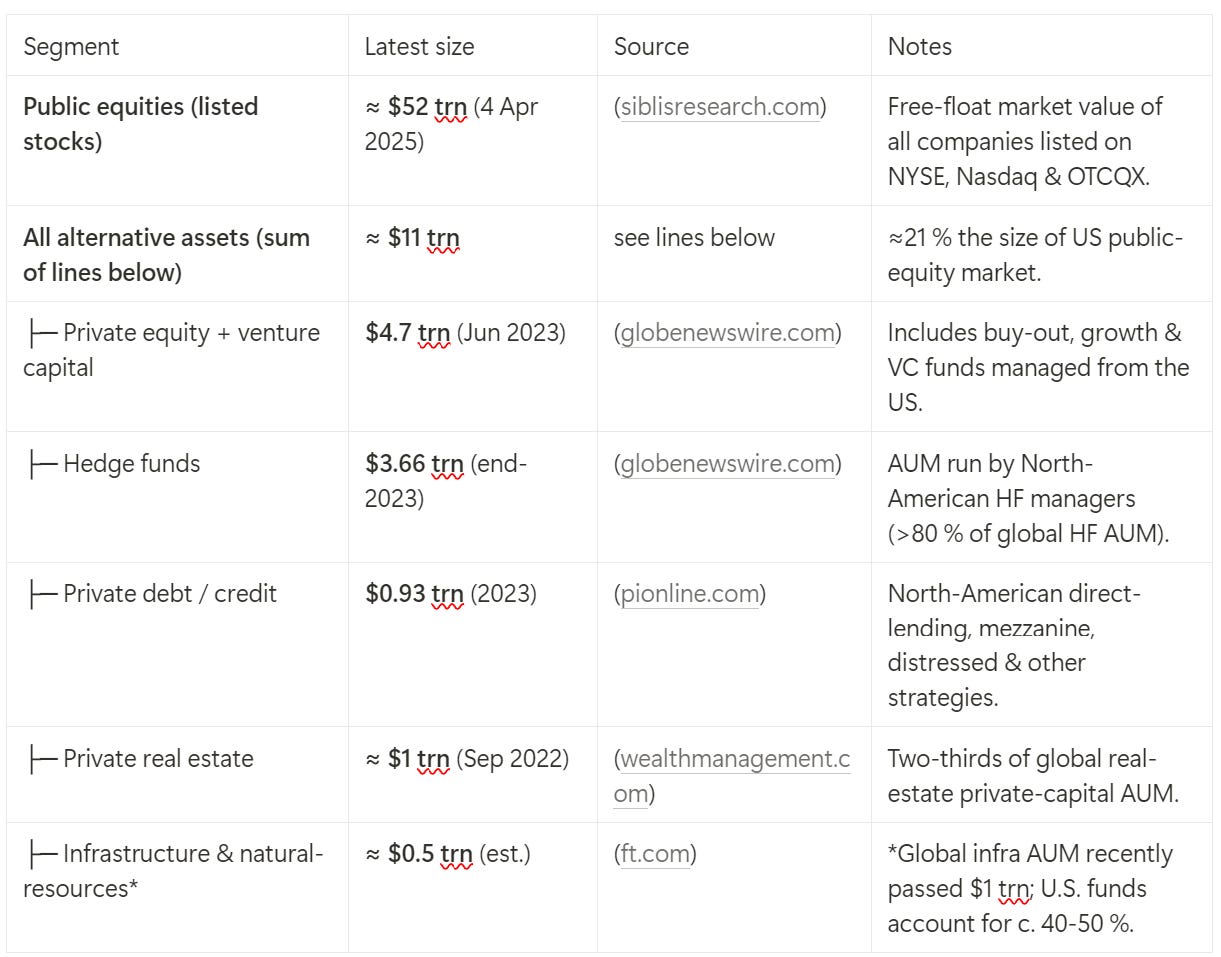

Public equity = ~$50T

• 60%+ of adults say they own stocks

• 40% of total U.S. equity market cap is held directly by householdsAlts = ~$11T

• Alts are just 5% of advisor-client portfolios (vs. 25% for institutions)

Public markets have shrunk. In 1996, there were 7,300 public companies. Today? 4,300. Meanwhile, PE-backed companies have grown 5x in 20 years.

From July 2020 to June 2021: Private offerings raised $3.3T vs. IPOs raised just $317B.

Nearly 90% of U.S. companies with >$100M revenue are private. Companies are also staying private longer — median IPO age went from 6 years (1980) to 11 (2021).

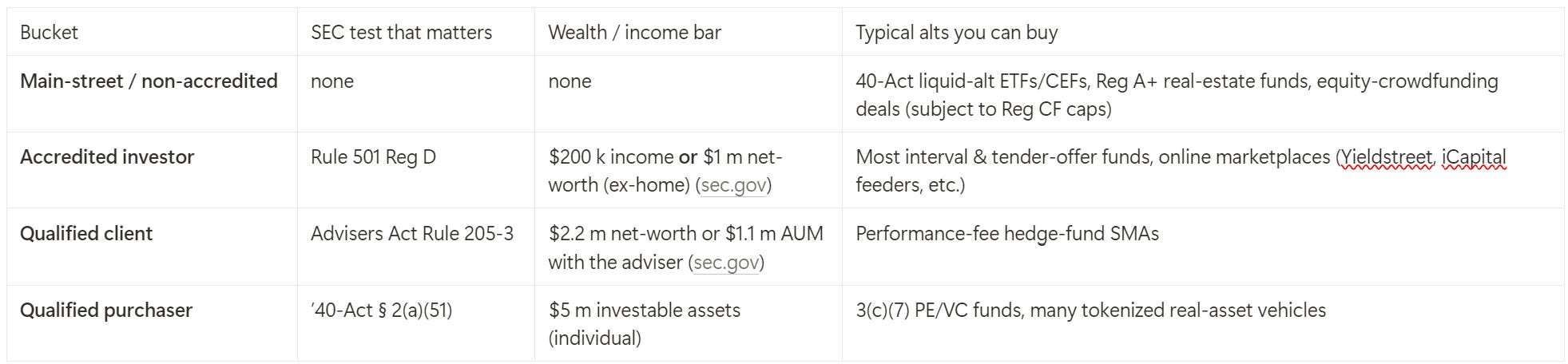

Despite this growth, private markets remain off-limits to most retail — largely due to the “accredited investor” rule: Net worth >$1M (excluding home) or Income >$200K/yr for 2 years. Only ~18.5% of U.S. households qualify.

To me, it’s inevitable that the 5% alts penetration will go up. The only question is how fast, when, and how.

Traditional (off-chain) players are inching forward. SCHW 0.00%↑ launched SAIS (Schwab Alternative Investments Select) in April 2025 — a curated shelf of PE, credit, hedge funds, and RE. For the first time, Schwab lets retail access illiquid alts directly. But only if you have >$5M in Schwab assets.

Many have asked: Why bother with tokenize? What can tokenization do that traditional platforms can’t? Esp. if SEC “loosens” their rules a little bit.

On paper, tokenization throws out all the buzzwords: Liquidity. Efficiency. Transparency. Fractionalization. Financial inclusion. 24/7 trading. Global reach.

But let’s be clear — tokenization doesn’t create a new asset class.

The same regulators still govern the underlying assets. The on-chain wrapper changes how we access them, not what they are.

So what’s the big deal?

Yes, it’s fair to ask:

– Is 24/7 trading really that important?

– Couldn’t the SEC just modernize traditional rails instead?

The reality is:

Alts have been off-limits to retail for so long — gated behind accredited or QP status — that most people just stopped asking/ looking for it. It simply feels remote & only for the elites

The subs onboarding is tedious af (weeks + documents) - almost impossible to be complete without a human advisor (again, only for the rich). The buying process is painful.

Alts lacks a real catalyst to really take off in the “real world”.

Tokenization changes that. Not by rewriting the laws. But by packaging alts in a way that finally makes sense to retail:

Fast onboarding

Lower minimums

Digital-native flows

Sometimes, all it takes to unlock demand is a selling point/ story & a better user experience.

If (still a big if) tokenization really takes off, here’s what my case study / investment documentation might look like a few years from now:

Industry tailwind: Rode the inevitable shift — alts penetration climbed from 5% to [_]% as access widened and demand finally met supply.

PMF via user experience: Nothing magical about tokenized assets themselves. But the experience? Night and day. What used to take a week of forms and wires got compressed into minutes inside a browser wallet. “Tokenized” sounded cool — and that was enough. Retail adoption ramped quickly [two years after 2025].

Smaller checks = wider reach: Tokenization cut back-office friction and cost. That brought minimum check sizes down — from millions to tens of thousands. Traditional wealth management is still bound by 3(c)(7) rules: max 2,000 qualified purchasers per fund. Keeping the ticket big helps avoid hitting that limit. But it also caps reach.

Off-chain: every new LP means forms, wires, statements, blue-sky filings.

On-chain: just a wallet + an API call.

(Bonus) Expanded eligibility under a friendlier administration: The SEC finally moved beyond wealth as a proxy for sophistication. “Accredited investor” got redefined to include anyone advised by a registered RIA or broker under Reg BI, or anyone who passed a standardized knowledge test.

Knowledge ≠ wealth. The rulebook caught up.

Adoption path:

Started with tokenized public equities (as a demo rail) → moved to alts.

Europe moved first → U.S. followed with regulatory clarity.

Everything snowballed from there.

Crazy? Maybe. But my case study’s already written lol.

Now just waiting for the disruptors to execute. :)

APPENDIX — A snapshot of tokenized alts in the U.S. today

1/ Same eligibility, smaller checks.

Tokenization doesn’t lower the regulatory bar — you still need to be accredited or a qualified purchaser for most PE/credit funds.

But it does meaningfully shrink the minimum investment: from millions down to tens of thousands.

Eligibility is a legal issue, not a tech one.

Sponsors choose an exemption (e.g., 3(c)(1) or 3(c)(7)), and the law sets the wealth bar — tokenization doesn’t change that.Minimums are dropping fast.

Example: Securitize cut a Hamilton Lane private-credit fund minimum from $2M to $10K, with fully digital onboarding and KYC.No shortcuts on compliance.

Tokenization doesn’t weaken legal tests — it just automates them. Platforms like Securitize and Anchorage handle KYC/AML and wallet whitelisting at sign-up, making the process instant and API-driven.

2/ Process is night-and-day.

What used to be a week of back-and-forth — subscription docs, wire transfers, email confirmations — now takes minutes inside a browser wallet.

Redemptions settle to the same wallet in stablecoins or new fund tokens.

3/ Operational alpha is real.

Managers like Hamilton Lane and BlackRock aren’t just chasing buzz — they see real savings and broader reach.

Smart contracts replace 3–4 legacy vendors

Capital flows go from multi-week to same-day

Administrative costs drop by ~50%

This is why large PE firms are already launching tokenized evergreen feeders — even before any regulatory changes to investor eligibility. As SEC custody rules evolve and custodians support wallet infrastructure, expect this momentum to accelerate.

APPENDIX — Main Street vs. the Qualified Purchasers (“QP”)