Prediction Markets | 2026.06

With the World Cup around the corner, there is growing anticipation around how prediction markets will perform.

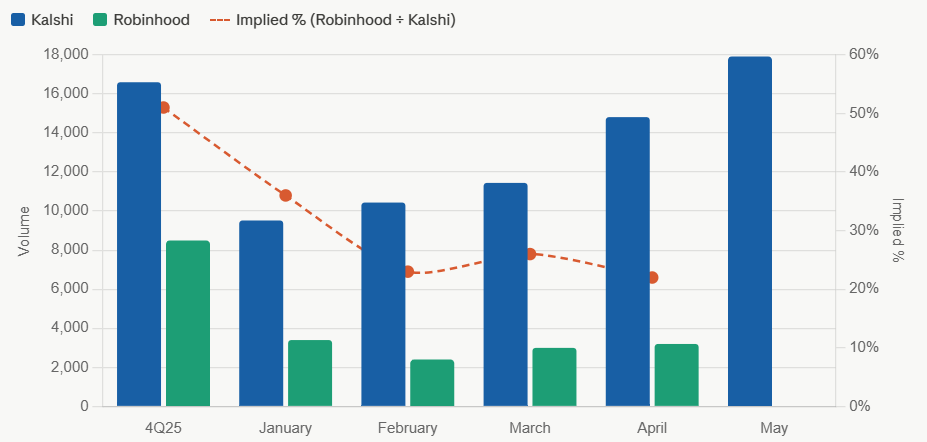

YTD, the most notable changes have been:

1) $Kalshi’s stellar growth, with volume up roughly 90% from January to May; and

2) the growing divergence between $Kalshi and $HOOD’s prediction-market volume.

$HOOD used to represent roughly 50–60% of $Kalshi’s implied volume. That ratio has declined every month this year, falling to 22% by April 2026. $HOOD’s own prediction-market volume has been essentially flat YTD.

Source: HOOD monthly disclosed by company; Kalshi daily from public data tracking

At first glance, one might assume $Kalshi is intentionally directing volume away from $HOOD and “cutting $HOOD out.” But this is more of a pull model than a push model. In my view, the issue is more likely on $HOOD’s side.

There are a few possible explanations.

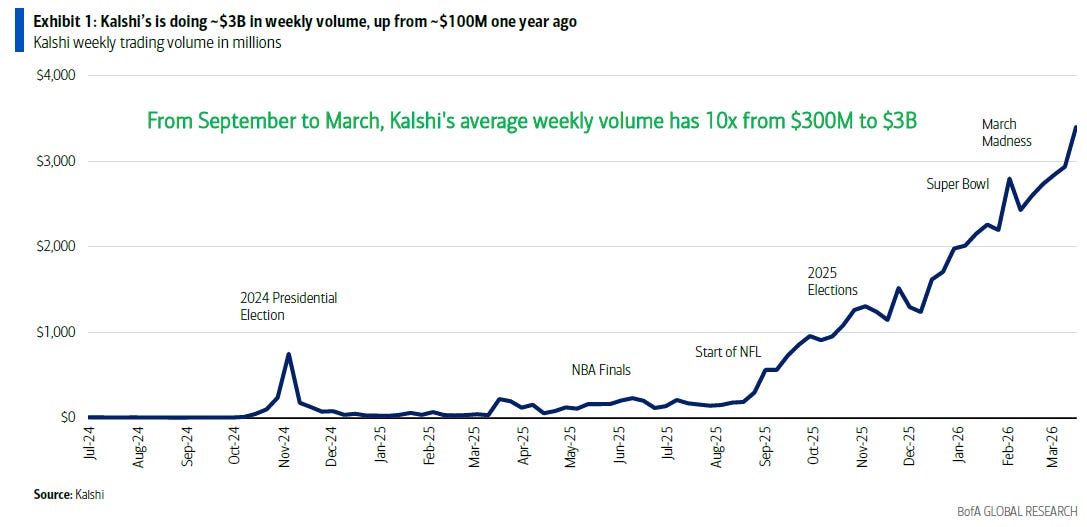

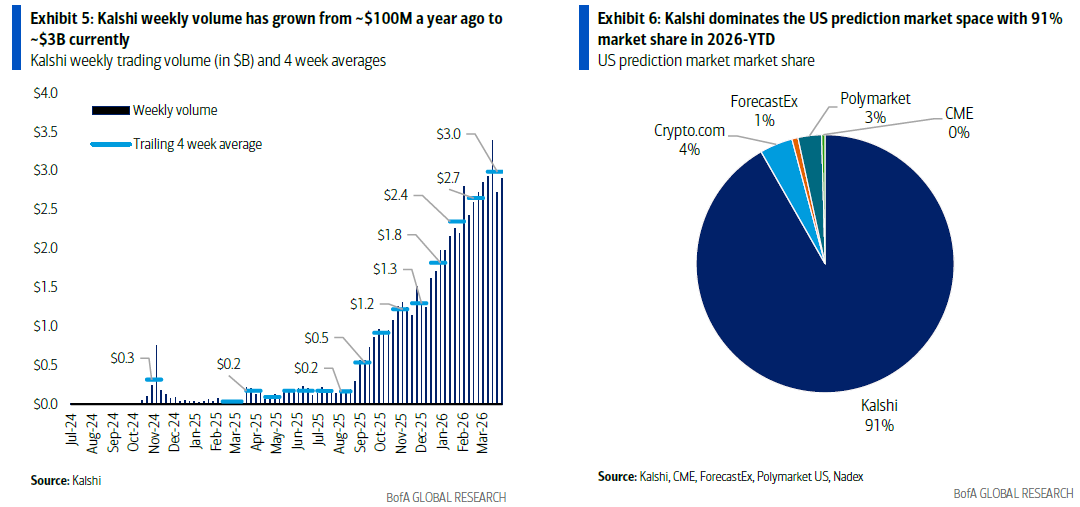

First, $Kalshi has added new distribution and exchange partnerships, including Coinbase.

It is estimated that $Kalshi is now generating 60%+ of volume from its own platform/API, with the remainder coming from broker partners including $HOOD, Coinbase, PrizePicks, and others. $Kalshi went viral in 1Q, helped by strong momentum around the Super Bowl and March Madness.

Second, $HOOD’s current product supply is more limited, while $Kalshi has seen growth in non-sports contracts.

$HOOD remains very sports-heavy.

$Kalshi is also still sports-heavy, with sports representing roughly 80% of YTD 2026 volume. But $Kalshi’s non-sports share has increased from 9% in December 2025 to roughly 20% by March 2026.

Looking forward, $HOOD’s own prediction-market JV appears to have come online right before the World Cup.

Rothera recently went live, likely in late May or early June 2026, and $HOOD has now begun routing at least some prediction-market flow to Rothera. Rothera is operated by the $HOOD/SIG JV. $HOOD is the controlling partner, SIG provides liquidity, and MIAXdx provides the CFTC DCM/DCO infrastructure.

On unit economics, the current $Kalshi-distributed-through-$HOOD model appears to be: the customer pays 2 cents, with 1 cent going to $HOOD and 1 cent going to $Kalshi. With the new JV, $HOOD can technically capture more of the economics. The open question is whether $HOOD will keep that incremental margin, or use a better and cheaper product to acquire customers — consistent with how the company has competed in other verticals.

The World Cup will be an important test. It remains to be seen whether $HOOD becomes more aggressive on customer acquisition and product promotion around the event.

Medium to long term, $HOOD likely needs to broaden its prediction-market product offering beyond sports. If the company wants to close the gap with $Kalshi, distribution alone may not be enough. The product surface area needs to expand.

h/t BAML

Source: BAML, Kalshi: Trade on everything, 04/08/2026

https://robinhood.com/us/en/newsroom/the-world-cup-is-now-trading-on-robinhood-and-rothera/

“Trading prediction markets on Robinhood now costs less than ever, with some of the most competitive fees in the industry. On June 1, we introduced a new pricing model where commission fees change based on the price of the contract and the size of the order, with lower fees at the extremes (contracts priced near $0.01 and $0.99) and never exceeding $0.01 per contract. We’re also now giving Robinhood Gold subscribers an even better deal, charging up to 50% less per trade in commission fees compared to non-Gold customers, and offering savings of up to 95% compared to our old pricing structure. Exchanges typically charge an additional fee, which varies by exchange.”

The information presented in this newsletter is the opinion of the author and does not reflect the view of any other person or entity, including Altimeter Capital Management, LP (”Altimeter”). The information provided is believed to be from reliable sources but no liability is accepted for any inaccuracies. This is for informational purposes and should not be construed as investment advice or an investment recommendation. Past performance is no guarantee of future performance. Altimeter is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. Altimeter and its clients trade in public securities and have made and/or may make investments in or investment decisions relating to the companies referenced herein. The views expressed herein are those of the author and not of Altimeter or its clients, which reserve the right to make investment decisions or engage in trading activity that would be (or could be construed as) consistent and/or inconsistent with the views expressed herein.

This post and the information presented are intended for informational purposes only. The views expressed herein are the author’s alone and do not constitute an offer to sell, or a recommendation to purchase, or a solicitation of an offer to buy, any security, nor a recommendation for any investment product or service. While certain information contained herein has been obtained from sources believed to be reliable, neither the author nor any of his employers or their affiliates have independently verified this information, and its accuracy and completeness cannot be guaranteed. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, timeliness or completeness of this information. The author and all employers and their affiliated persons assume no liability for this information and no obligation to update the information or analysis contained herein in the future.