Digital Banks | 101

Not all neobanks are created equal.

They share the same ambition:

→ Become your primary bank

→ Become the super app for your financial life

But how they get there looks very different

Where They Started

Chime

Launched as a checking account alternative for working-class Americans underserved by legacy banks.

Value prop: get paid early, no monthly fees, no overdrafts, no BS.Cash App

Began as a peer-to-peer wallet.

Gradually expanded into debit cards, stock trading, Bitcoin, and buy-now-pay-later (Afterpay).

Feels more like a “super app” for money management.Revolut

Born in Europe to solve one problem: real-time FX without outrageous bank fees. “Stop getting fleeced on holiday.”

Today, it offers banking, investing, business accounts, and travel insurance — all in one app.

Are They Winning “Primary Bank” Status?

Chime

67% of its 8.6M active users use it as their main financial account

Over half of those users set up direct deposit

Best in class on engagement — arguably the wage bank for a big slice of America

Cash App

2.5M users receive direct deposit (as of Dec ‘24), which is ~4% of the 57M MAU

Revolut

Pushing hard into salary deposits — added local IBANs, “Salary Sorter,” etc.

~£480 average monthly inflow per user vs. ~£2,100 UK median salary, which implies most users still split finances: legacy bank (bills) + Revolut (spending, investing)

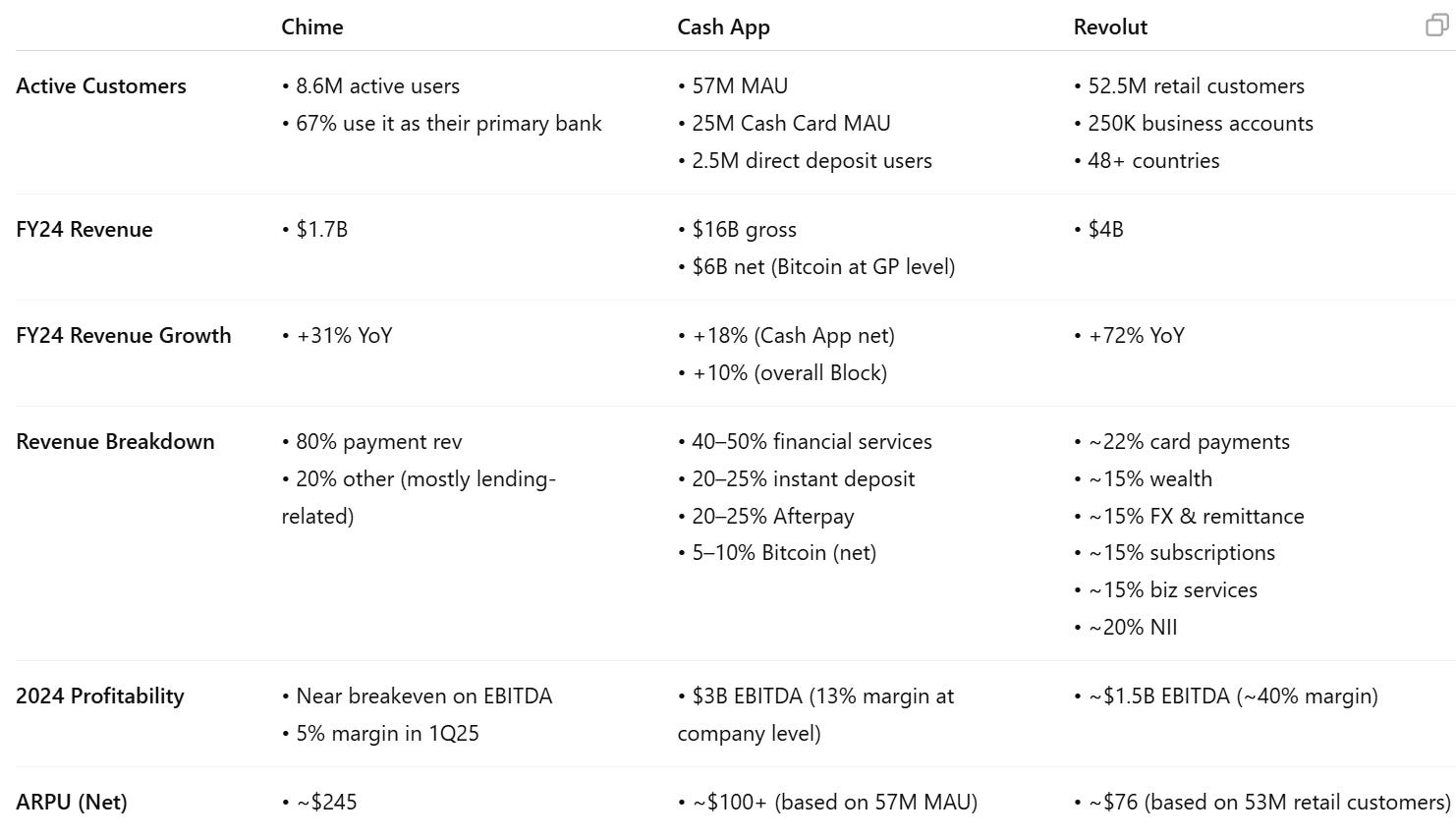

Neobank Comparison Table

Source: financial reports; IPO S1 (Chime)