AAPL | 2026 Setup

AAPL is the last name in the Mega 7 to truly “show its cards” on AI. The setup here is interesting, with catalysts on both fronts:

Hardware

Rumored foldable iPhone launch (Sept 2026)

Rumored iPhone 20th anniversary launch (Sept 2027)

Software / AI

“New Siri” launch rumored for spring 2026

What adds to the intrigue is that Apple has recently gone through a set of major internal reorganizations. Big reorgs sometimes (not always) lead to upside surprises - tighter focus, better execution, faster decision-making.

Beyond the CFO and COO changes in 2025, the most consequential shift was the retirement of John Giannandrea and the realignment of the AI/ML org under Craig Federighi’s Software group. As part of this move, Siri leadership was shifted away from JG to Mike Rockwell. (source: https://www.theverge.com/news/633358/apple-replace-siri-leader-john-giannandrea?utm_source=chatgpt.com)

New Siri

Apple plans to use a custom Gemini model (reported at ~1.2T parameters) running on Apple’s PCC servers to power an upgraded Siri, alongside Apple’s own models for certain tasks (suspect that’s the small model on the edge).

Reuters+2From the outside, this appears largely “outsourced” to Gemini, with Gemini focused on planning, summaries, and web knowledge. Longer term, Apple might need to own a more complete in-house model. But this upcoming Siri launch looks more like a pragmatic step to “get it working,” with the emphasis on product experience rather than model ownership.

Expectations for this launch are relatively muted, which leaves room for upside if execution is better than feared.

Gemini Deal & Implications for GCP (updated: 1/21/2026)

According to Mark Gurman:

1/ A model coming to Siri (Spring)

Implications: Running on AAPL’s servers (PCC). So it’s not really GCP consumption.

2/ Revamped Siri Chatbot known as Campos (Fall)

Apple Inc. plans to revamp Siri later this year by turning the digital assistant into the company’s first artificial intelligence chatbot, code-named Campos. The chatbot will be embedded deeply into the iPhone, iPad and Mac operating systems and replace the current Siri interface, allowing users to summon the new service by speaking the “Siri” command or holding down the side button. The new approach will go well beyond the abilities of the current Siri, with features such as searching the web, creating content, generating images, and analyzing uploaded files, and will be integrated into all of the company’s core apps.

Implications: It’ll be likely be powered by Gemini running on Google’s own TPUs and cloud infrastructure, meaning it’s a far more powerful model than the one coming to Siri this spring. This should be GCP revenue.

Source:

The $1B License Fee (The IP Tax)

As reported by Bloomberg and others, Apple is paying roughly $1 billion per year just for the right to use the Gemini “weights”.

Margin Profile: ~90%+. This is “clean” software revenue. Google has already trained Gemini; letting Apple use it costs Google almost nothing incrementally.

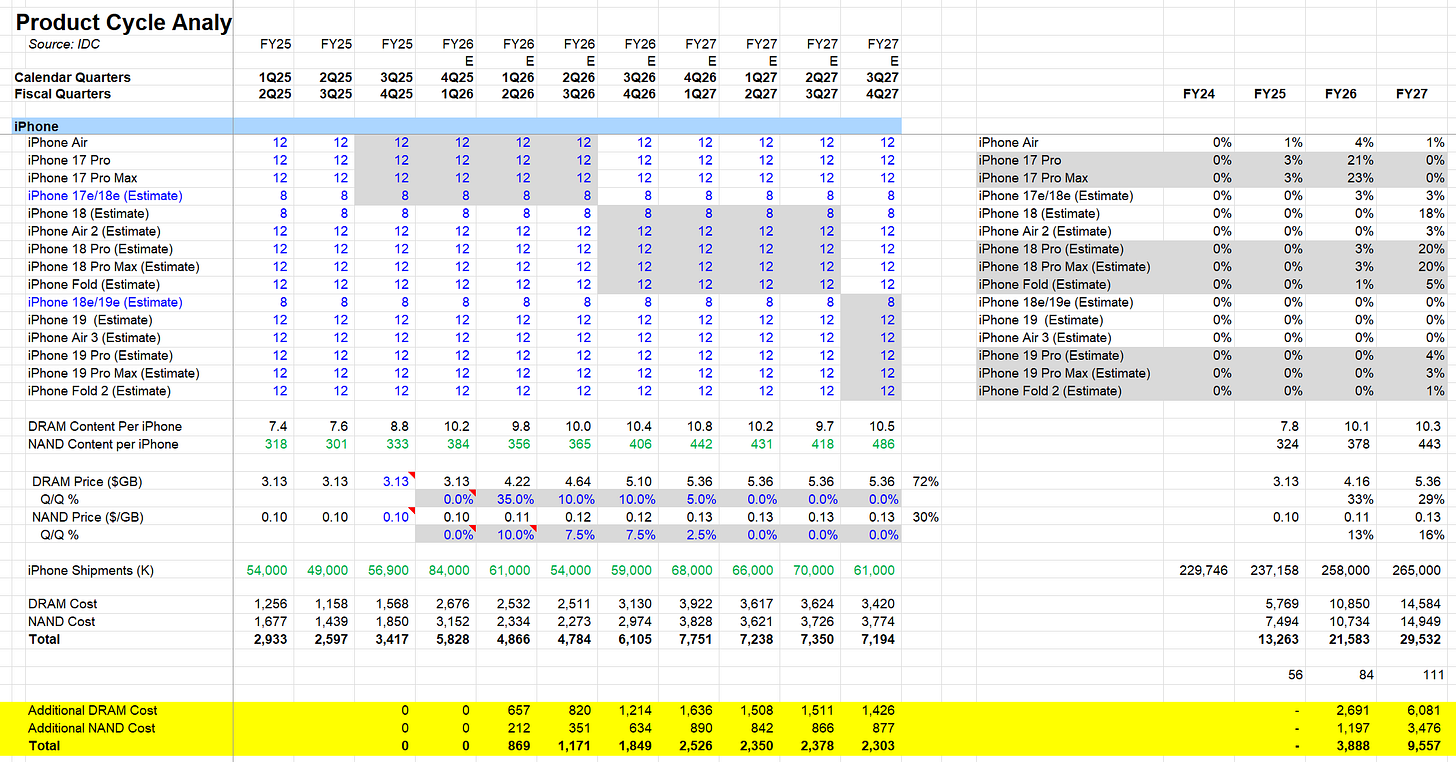

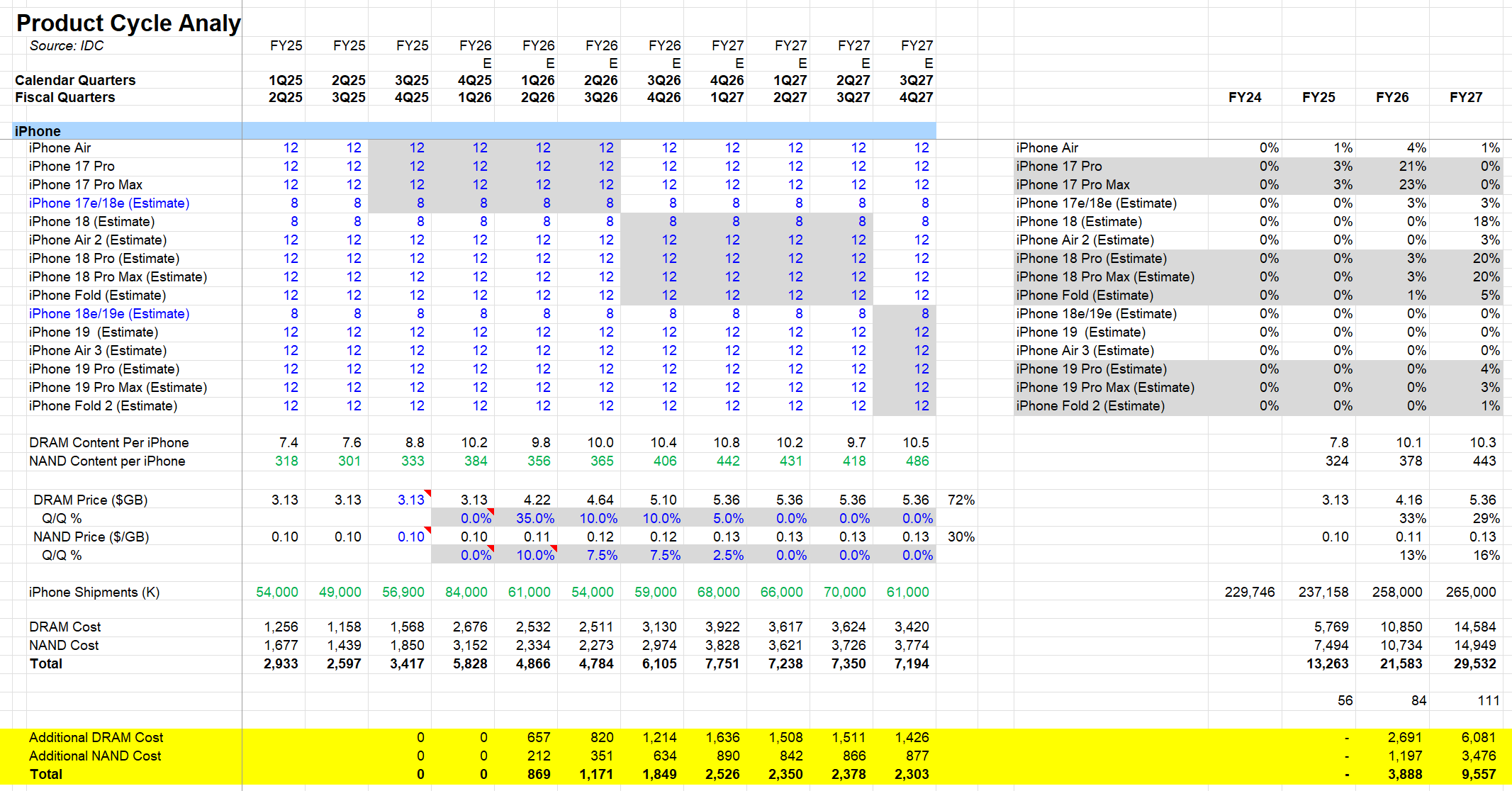

Hardware

Foldable

Consensus expectations for a US launch MSRP cluster around $2,000–$2,500.

mingchikuo.craft.me+2MacRumors+2This is broadly in line with Samsung and Google foldables at ~$1,799–$1,899.

Apple’s foldable is expected to remain a smaller part of the overall iPhone 18 mix.

Supply chain checks suggest 15–20m foldable units shipped in FY27, or <8% of total mix.

Even at a smaller mix, this could still drive 15%+ ASP uplift in FY27E.

Margins

The MS team has done solid work here. With DRAM pricing expected to go up by ~70% and NAND up ~30%, memory could move from ~10% of COGS to ~20%.

That implies a ~1–2% drag on gross margin.

Apple likely will not be able to pass this through to end customers during the iPhone 17 cycle (limited precedent), implying a reset around the iPhone 18 launch.

Timing-wise, supply chain checks suggest the margin impact could show up as early as 1Q26, leaving open whether this is reflected in the 4Q25 guide.

Source: MS model

Net-Net Setup

This looks like a setup where the stock is waiting for a reset in margin expectations.

From there, the key question is whether Siri lands better than feared, now that it is largely “calling Gemini for everything” in its first iteration.

The hardware cycle is constructive but not as extreme as some narratives suggest - not the entire iPhone 18 cycle is going to be foldable, so ASP and volume upside are capped.

There is also potential noise from Google Pixel (expected Pixel 11 launch in 2H26), OpenAI hardware, and other entrants.

Overall, this does not feel like a “Google 2025”-style turnaround that is already baking in. Taking into account the stock’s seasonality into consideration, it looks more like:

Margin reset pressure likely persists into Feb/March. From there, the stock should work higher into the Siri launch and the iPhone 18 cycle in September, with the primary upside window running from roughly March through September.

If memory costs prove more punitive than expected, that could disrupt this pattern. However, even in that scenario, the iPhone 18 launch should fully reset the margin impact. Apple typically does not raise prices mid-cycle, but instead adjusts pricing at the start of a new product cycle - which would apply with iPhone 18.

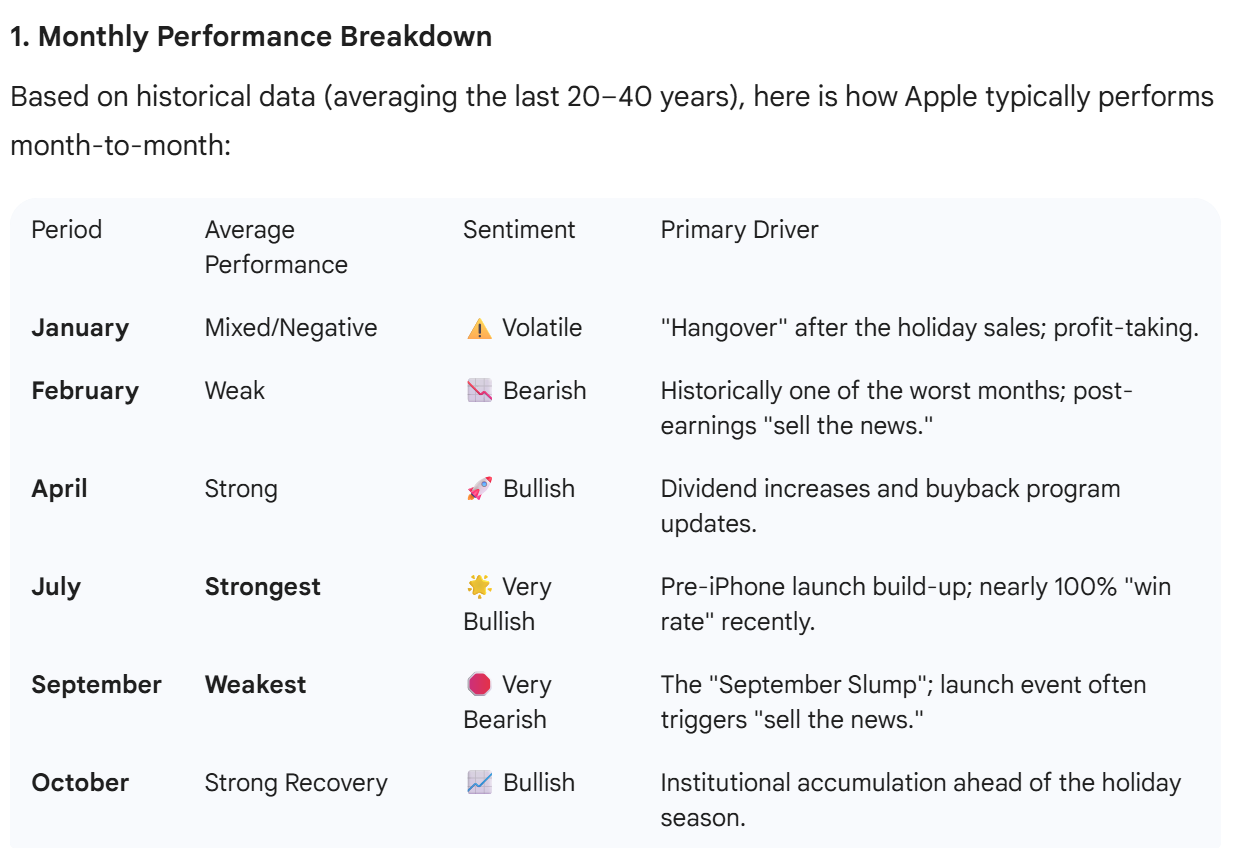

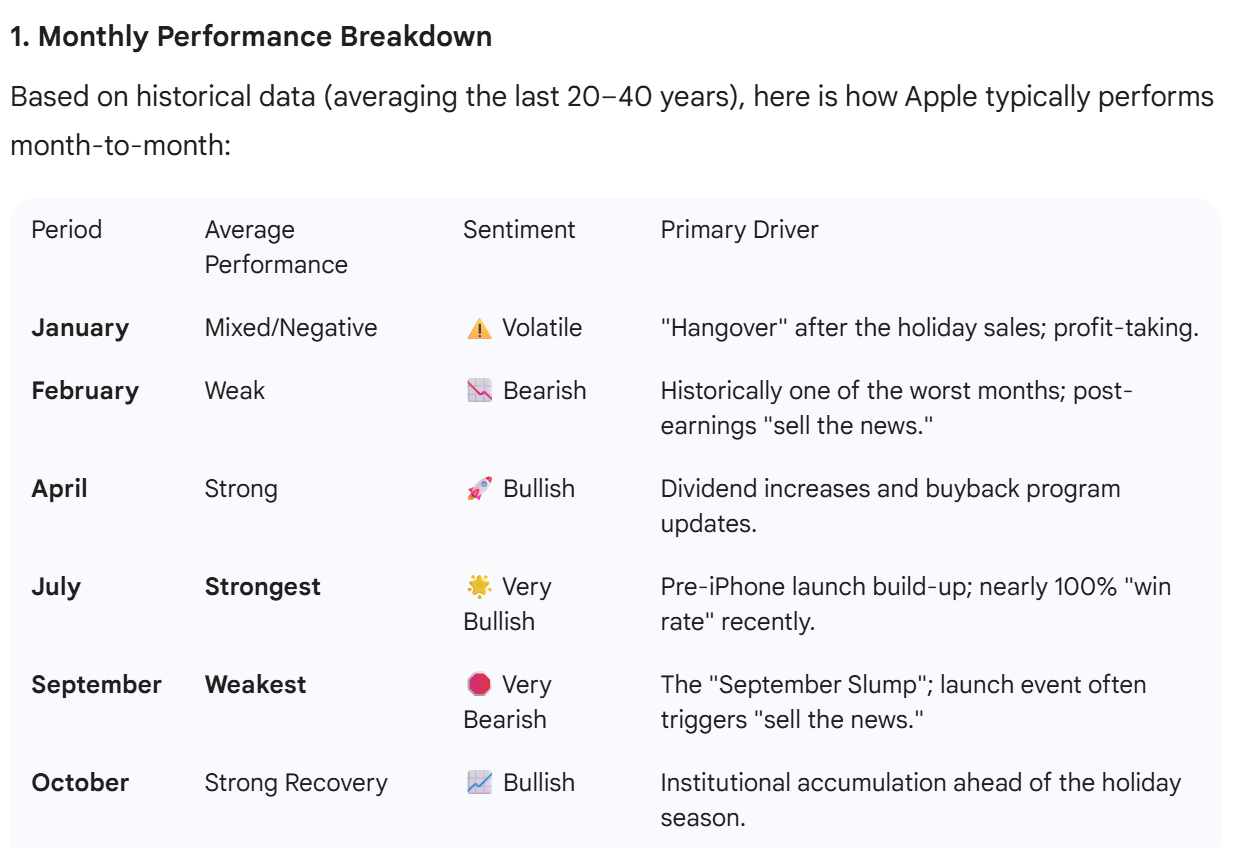

Seasonality

AAPL remains a stock with very clear seasonality. Per Gemini: “Buy from March to Sept” has been the winning trade

The Summer Run (June–August): Markets begin pricing in the new iPhone launch and back-to-school demand. July has historically stood out, with some data sets showing positive returns in 100% of the past 15 years.

The September Correction: Apple often peaks in late August or early September. Once the new iPhone is revealed, the stock frequently undergoes a valuation reset as speculators exit.

The Year-End Rally (October–December): Driven by holiday sales expectations and year-end window dressing, where Apple remains a core holding for many managers.